Isn’t it right? Isn’t it that diversity of talent and skillset and divergence of opinions are recipes for success and fuel growth? I get it, the ‘same page’ principle is what people like to tout and promote but that shouldn’t be and can’t be before ideation, before finalizing strategy, before working out what should be worked upon!

At the executive table, difference of opinion is required to be treasured because creativity is not owned by anyone in particular. An idea, a solution to a problem, a plan could come from anyone. The odds of that happening are equal. And isn’t that what teamwork is about? And especially when it is said, teamwork makes the dreams work?

Or is it that entrepreneurs believe it is their vision that all their employees working as a team need to realize? Why do they then hire people as head of marketing, head of business development, head of strategy and those at research and development? Surely, they can assume all these roles if it is them who has to do all the thinking and ideation.

Maybe for running numbers, doing research and analyses and drafting reports but no thinking and ideation. But then they can be easily replaced by tech. But somehow, these positions continue to exist to this day, even with tech entities! So maybe, they’re actually there for some ideation, creation or even critique.

Because entrepreneurs do need thinking heads. They do need people around who can generate ideas. People who could find and suggest ways and means to turn a vision into reality. People who could also find and suggest alternates. People who could ascertain viability. And people who could simply be promoters.

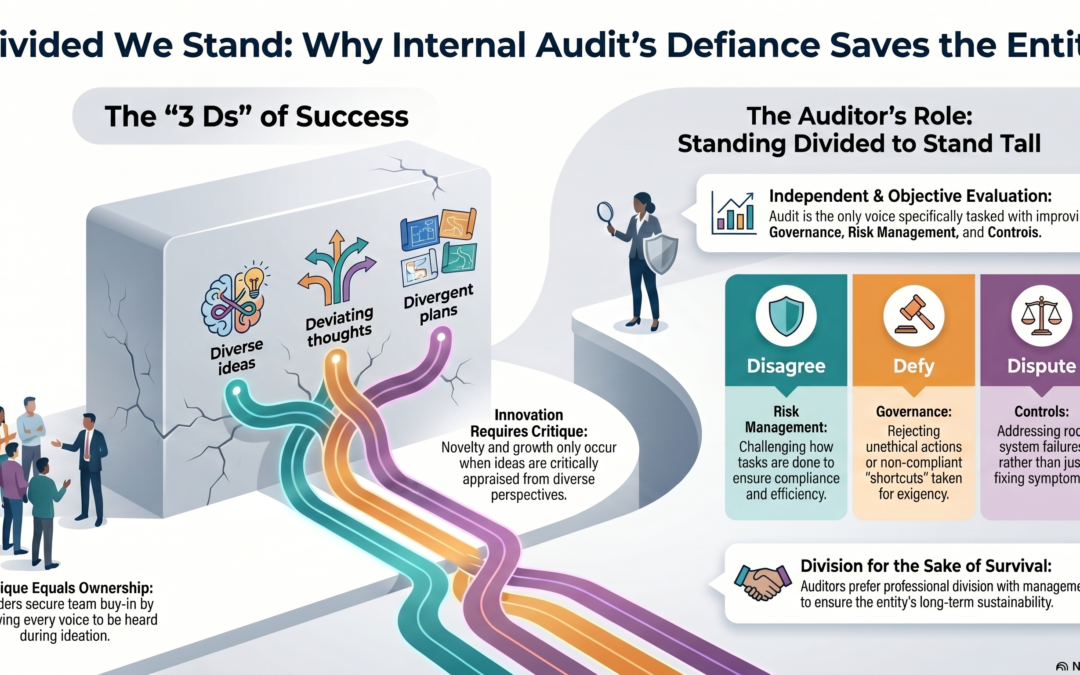

And when entrepreneurs become leaders or aspire to be one, they invite criticisms directed at their vision aiming for its perfection. And also, because a leader takes everyone along. And the best way of doing it is to secure the team’s ownership / buy-in. Ownership, that comes when everyone gets a chance to make a bid (be heard).

Critique is imperative. It allows an idea, a plan, a strategy to be seen in an entirely different perspectives. Perspectives that might not even have been thought of before! In terms of viability, impacts, by-products, threats and opportunities. These won’t come to the fore, unless people are allowed to share their thoughts, especially divergent ones.

The type of thoughts that neither conform nor subscribe to any particular vision. And the type that would critically appraise, recommend tweaks and even offer alternates. A thought deviating from the generally accepted norm and the typical thinking pattern. Thoughts not expected from king’s men but from a teammate willing to make a distinctive contribution.

Indeed, contributions are meant to be distinctive. If these aren’t, there’s no point in having skilled resources to do the job. One can simply have the tasks automated. How one accomplishes a task and its objectives is how one is identified as having a skill set and its uniqueness.

And then come the entrepreneurs themselves. Do they always get successful by pitching and selling an age-old established idea or something entirely new? What is that novel idea and first movers’ advantage? What do they take, a path beaten or a path less trodden? Do they succeed by the standardization of their thoughts or the novelty of their ideas?

So, if the novelty of the idea is what assures the entrepreneur of its success, why and how novel ideas and thoughts could be shut? The novelty made the entrepreneur known, keeping open to these and 44practicing these is how the entrepreneur will continue to be known. Because that’s exactly how we remain ahead of the curve and reap those dividends that others can only have a look at when we’re done.

And if the 3 Ds; Diverse ideas, Deviating thoughts and Divergent plans are the means to ensure distinctive success, how could this be any different when faced with the disruptive energy of internal audit? Isn’t internal auditing all about the 3 Ds? Aren’t these the hallmark of what we stand for and what we insist upon? Or do we represent a lot more than these 3 Ds?

Yes, we’re disruptive. But as I’ve covered it already it’s all for the greater and ultimate good. There’s this one ‘D’ about us that encapsulates all other Ds. We Differ! And we’re required to Differ. I mean that’s exactly how internal auditing works. We aren’t expected to agree unless it’s about the fulfillment of the objectives of the entity we’re serving.

And yes, that’s the only objective that we could agree on, but in our own professional approach guided by the requirement of evaluation and improvement in Governance, Risk Management and Controls (GRC). In that respect, our modus operandi is that,

- We Disagree on how something has been done or not done, because something needed to be done in a compliant, adequate, effective and efficient manner to ensure the objectives were accomplished in the manner intended but they weren’t. RISK MANAGEMENT

- We Defy the common and perfectly entrenched management approach of accepting any unethical, non-compliant and violative action as a matter of exigency. GOVERNANCE

- We Dispute the management’s understanding about resolving an issue if it does not help evolve and improve the system but only improves the symptoms. CONTROLS

- We Dissociate ourselves from any scheme management insists upon implementing to benefit themselves that might or might not be detrimental to the entity’s objectives but might cause our judgment to be clouded and independence to be impaired on evaluating that very scheme.

- We Dissuade management’s efforts to subdue, undermine, belittle and ignore our findings and value addition efforts through perseverance leaving them no option but to evolve and improve.

It’s no wonder we usually find ourselves up in arms against managements, especially those that do not have the appetite to deal with us professionally. Divisions between us and the managements do not bother us a bit and they shouldn’t because that’s how it’s meant to be.

It’s our duty to remain mindful of why the entity has invested in us, even if out of a statutory or regulatory compulsion. It’s because we, being the only independent and objective voice amongst an entity’s team, are required to evaluate and cause to improve the GRC systems.

It’s not our problem if our evaluations earn us foes rather than friends and we’re considered adversaries rather than advisors. The independent and objective evaluations and improvements in GRC, we’re responsible for ensure the entity’s sustainability and growth!

If we start toeing the management’s line, our outlook may be united but the entity we’re serving won’t survive it. In order to ensure the entity continues to stand, it needs to have internal auditors who defy the management when it’s stewardship is at odds with the auditor’s commitment to the entity.

It is thus in the management’s interest that it does not opt for a continuing collision course with us because we prefer divisions with the management for the sake of entity’s survival.

Instead, what it should opt for is a course correction!

We stand Divided!